Navigating unprecedented economic shifts to find strategic advantage.

With our combined decades of experience in global finance, tax advisory, and corporate strategy, we have navigated countless economic cycles. Yet, we can say with confidence that the times we are in now are truly epic. The convergence of domestic tax incentives/changes, evolving tariff regimes, U.S. and global international tax changes, and global economic pressures is creating a landscape unlike any we have witnessed. For financial executives, this isn’t just another cycle; it’s a fundamental rewiring of the rules.

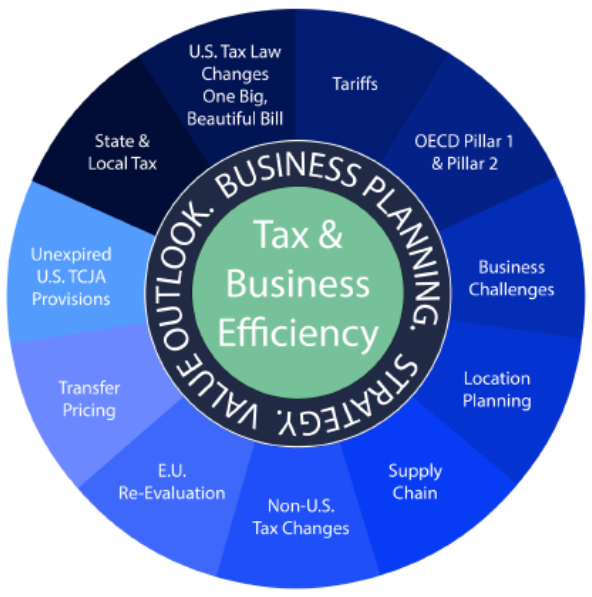

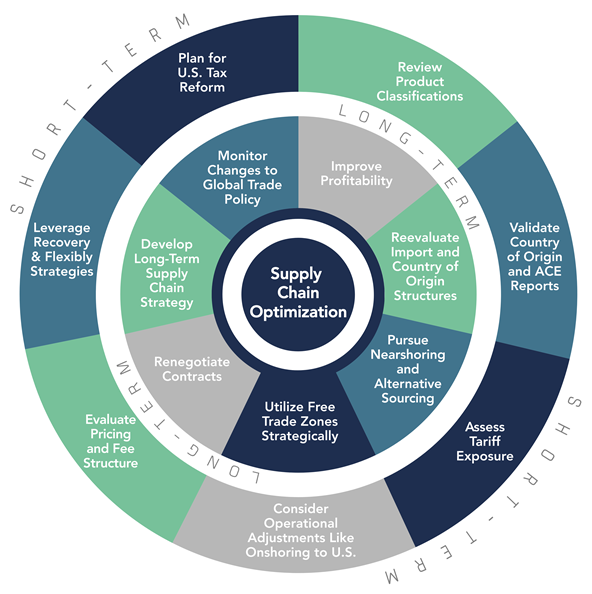

From our vantage point, working with both large multinationals and closely held businesses, we see these shifts having a direct and immediate impact across the board. The decisions business leaders make—or fail to make—in response will have profound implications for cash flow, profitability, and long-term competitive positioning. This is a time of action and strategic decisions need to be made. The complexity of the decision making is illustrated in the following chart that highlights the decision process.

Our goal here is to cut through the noise and share what we’ve learned from the front lines. This is about moving beyond reactive compliance and toward a proactive strategy that turns complexity into opportunity. For CFOs and senior finance leaders, this is a moment to guide the business through uncertainty and create lasting value.

Understanding the intersection of tax, tariffs, and business planning are key to successful financial outcomes.

The Global Chessboard: Understanding the Tariff Tension

The current tariff situation, particularly policies enacted by the U.S., has introduced significant tension into global trade. It’s no longer enough to simply know a tariff has been imposed on a specific good. As leaders, we must monitor the global reaction. How are other countries responding? How do these policies align—or clash—with international agreements like the OECD’s minimum tax framework?

Understanding where your company is now in light of tariffs and the upcoming Supreme Court decision on reciprocal tariffs is critical to planning. As the chart below indicates, decisions need to be made on onshoring, export centers, coding and country of origin. These are a few of the key areas to consider.

For instance, we’re seeing the U.S. export tax rate for C corporations hover around 14%, which is just below the OECD’s 15% minimum tax. This small difference is not an accident; it’s a strategic position. It signals an intention to remain competitive while navigating a complex web of international standards. The key takeaway for financial executives is the need to stay educated on these global macroeconomic events. What happens in Brussels or Beijing no longer stays there; it directly impacts your P&L and your state tax liabilities. This isn’t just a matter for policy wonks. It’s a critical component of risk management and strategic planning for businesses of all sizes.

The Domestic Counterbalance: A New Incentive to Onshore

While tariffs create friction for global supply chains, recent changes in U.S. tax law are creating a powerful counterbalance. We’ve seen this become a pivotal planning point for our clients, from manufacturing firms to hospitality groups. Two of the most significant changes involve the treatment of Research & Development (R&D) expenses and capital depreciation.

Previously, the path of least resistance was often to conduct R&D wherever it was cheapest, which frequently meant overseas. Now, the calculus has changed dramatically. The tax code allows for the immediate and full deductibility of domestically performed R&D. In stark contrast,

R&D expenses incurred outside the U.S. must be amortized over 15 years. This is a

game-changer. The ability to instantly write off R&D costs creates a significant, immediate cash flow advantage. We encourage our clients and their teams to run the numbers and calculate the true, after-tax cost of offshoring these critical functions. When you factor in the time value of money, bringing R&D back to the United States becomes an incredibly compelling proposition.

Turning Capital Expenses into Cash Flow: The Power of Accelerated Depreciation

The second major incentive is the ability to fully and immediately depreciate new capital expenditures. This “100% bonus depreciation” is a powerful tool for improving the ROI on domestic investments. It allows businesses to recover the cost of machinery and equipment in a single year, freeing up capital that can be reinvested directly back into the business.

We recently saw this play out with a manufacturer of refrigeration units. The company needed a specialized machine that was only made in Europe and came with a hefty price tag, made even higher by tariffs. In the past, the multi-year depreciation schedule for such an asset would have

been a drag on cash flow. Today, the story is different. The company was able to treat the entire cost of the machine, including the tariffs paid, as a capital expenditure. They depreciated the full amount in one year. At the same time, they were performing R&D to adapt their products and processes for this new machine, and those R&D expenses were also fully deductible in the same year. The combined effect created an enormous cash flow benefit that fundamentally changed the economics of the investment. It transformed a burdensome cost into a strategic advantage.

Additional incentives in depreciation relate to construction of Qualified Production Property (QPP) where the cost of a manufacturing facility previously deducted over 39 years could qualify for immediate first-year depreciation. Although it takes some time to construct a plant, the incentive included in the One Big Beautiful Bill applies to construction started January 19, 2025 to January 1, 2029 and completed by January 1, 2031.

Interest expense limitations were also loosened to provide improved deductibility to debt financing.

From Theory to Action: A Practical Framework for

Financial Leaders

Understanding these concepts is one thing; implementing a strategy is another. As trusted advisors, we emphasize that everything is ultimately a business decision. It’s our job as financial leaders—both internal and external—to model the outcomes and help guide the executive team toward the most sound and profitable choices.

Here are a few practical steps we recommend:

- Review Your Contracts Immediately. Don’t wait for a problem to arise. Examine supply contracts to understand who is responsible for tariff costs. Review customer contracts to see if you have the flexibility to pass on increased costs. It may also be time to reconsider your INCO terms (International Commercial Terms) to better allocate risk.

- Model the Onshoring Opportunity. Task your team with a simple analysis: What would be the cash flow impact of bringing a portion of your foreign R&D activities back to the U.S.? The answer will likely surprise you and could spark a much broader strategic conversation about your operational footprint.

- Adopt a Multi-Tiered Supply Chain Strategy. You can’t change an entire supply chain overnight. We advise thinking in terms of short-term, mid-term, and long-term planning. In the short term, you might need to absorb costs. Mid-term, you should be actively seeking alternative sourcing options. Long-term, you may be looking at significant shifts, like new construction and assembly operations in different regions.

Looking Ahead: A Call for Proactive Leadership

The economic, tax, and trade policies we see today are not temporary ripples; they are tectonic shifts. This environment requires a new level of engagement from financial leaders. We are being called upon to be strategists, not just scorekeepers. The frustration many of us feel with late-breaking guidance from government bodies is real, but we cannot let it paralyze us. The burden falls on us to interpret, model, and act.

We see it every day: the greatest risk is inaction. By embracing the complexity and understanding the interplay between global pressures and domestic incentives, we can protect our organizations from risk. More importantly, we can uncover powerful opportunities for growth and value creation. It’s about proactive, value-added advice that prepares businesses not just for next quarter, but for the next decade.