You’re walking through a mall when you see a sign—“Flash Sale! 50% Off for the Next 2 Hours!” Suddenly, something you weren’t even considering buying feels urgent. The deal is right there, but only for a short time. You don’t want to miss out.

We see these kinds of temporary incentives everywhere. Retailers use flash sales to clear out inventory quickly, banking on urgency to drive purchases. Credit card companies push sign-up bonuses, offering cash back or miles if you spend a certain amount just after signing up. Grocery stores use loss leaders, pricing products below cost to bring customers in the door, knowing they’ll likely buy more profitable items once inside.

This is the idea behind how SPIFs (Sales Performance Incentive Funds) work in B2B sales: Sales reps are incentivized with extra cash or bonuses to push a specific product, land deals faster, or focus on a strategic goal for an immediate and brief time. Like the incentives above, SPIFs are aimed at driving sales that wouldn’t happen otherwise. At its core, this isn’t just about sales—it’s about behavior. But as with retail promotions, the big question remains: Do they drive real, incremental value, or are they just an expensive way to accelerate sales that would have happened anyway?

In B2B sales, SPIFs are seen as a common tool to solve business challenges—from accelerating pipeline to pushing new products. But too often, they do more harm than good, pushing for short-term results at the cost of long-term value. The problem? SPIFs are rarely designed with the business’s best interest in mind and end up costing the firm more than necessary. If more companies approach SPIFs with an owner’s mindset, these incentives could improve financial performance and shareholder value instead of undermining it.

We’ll explore why and how SPIFs are used, where they succeed, and—more importantly—where they fail. Our objective approach to SPIF design is based on 5 key factors. This approach helps prevent firms from overspending and ensures that each incentive provides the right tool at the right time. Because while a flash sale disappears when inventory is gone, a poorly designed SPIF can leave a company with unintended consequences long after the commission checks are cashed.

SPIFs are widespread in B2B sales, largely because of conventional wisdom about their effectiveness.1 When well-designed, SPIFs can deliver stronger short-term performance focused on a specific goal. But because SPIFs are paid on top of base variable compensation, they’re inherently more expensive than the status quo. So by design, they always increase incentive compensation costs. SPIFs are typically paid out on all qualifying sales but, in most cases, some of those sales would have happened without the SPIF. This means companies are almost always overpaying to some extent—the challenge is estimating how much. This makes SPIFs difficult to evaluate.

A company will have a natural—or expected—level of pre-SPIF sales. But most SPIFs pay out on all qualifying sales, combining expected and unexpected performance. To evaluate SPIF impact properly, firms must first estimate expected sales without the SPIF—and then answer two tough questions:

- What’s the likely sales range without the SPIF, and is that enough to meet the goal?

- What’s a realistic estimate of incremental sales from a SPIF-driven team?

These questions are tough to answer because sales outcomes are influenced by many overlapping factors—like seasonality, the time of year (e.g., end-of-quarter surges), and external forces impacting customer demand.

This is why it is important for firms to set a specific, challenging and incremental sales objective for the SPIF. It’s hard to hit the target if you don’t know where to aim. A goal that’s too broad can be expensive, as it generally leads to paying out on sales that would have happened anyway. But a goal that is too narrow may not engage enough of the sales team and can also undermine the SPIF’s perceived rarity. The idea is that a targeted SPIF nudges reps toward specific goals, driving quick wins.

SPIFs also help align sales focus with business needs, such as spotlighting underperforming products or redirecting attention to strategic priorities. Their temporary nature makes them more flexible than permanent compensation changes. In competitive markets, they help keep sales teams engaged and avoid stagnation. And when long-term plans fall short, SPIFs can provide a temporary jolt to sustain momentum.

Firms need to take care to ensure these temporary jolts do not become permanent fixtures. The longer the SPIF is in effect the longer the meter runs, racking up additional expense. As sales teams get more comfortable promoting aspects of the SPIF the need for the additional incentive diminishes. At some point the desired behavior becomes embedded, and by then the SPIF should be long-expired. But sometimes SPIFs linger past their point of impact. This adds cost and builds dependency.

However, not all SPIFs are deployed strictly for sales impact. Sometimes they’re used for optics—meant to signal action rather than drive results. Leadership may introduce a SPIF not because it expects big gains, but to show the board or executives that Sales or Product Management are being proactive. In high-pressure environments, SPIFs can serve as symbolic moves to buy time or create the appearance of traction.

The point is: not all SPIFs are strategic. Some are reactive. And not all uses are equally valid. While SPIFs can be effective when used thoughtfully, they’re often deployed out of habit rather than as part of a deliberative, data-driven strategy.

To be effective, SPIFs need a clear ROI rationale from the start. It begins with alignment. A SPIF should be built around a specific business goal—revenue, deal volume, product adoption, contract structure — and framed by reasonable expectations for the incremental increase in that metric.

A key question follows: what level of investment is reasonable to achieve that incremental gain? When companies frame the decision around the ratio of benefit to cost, they can determine a SPIF payout that makes sense. For example, a firm promoting a specific product can estimate the profit upside and allocate a portion of that to SPIF commissions. This works for firms focused on an upgrade program or sales of a newly acquired business. A company re-energizing a moribund sales team might target a certain revenue lift and budget an incremental commission that is meaningful but modest, ensuring success would meet both revenue and cost goals.

The mistake many companies make is approaching SPIFs backward. They begin by defining the payout, modeling total spend, and only afterward assess whether the results justified the expense. What’s often overlooked is the defining question: what level of improvement is needed to justify this cost? Without that foundational metric, SPIFs risk becoming an arbitrary expense rather than a strategic investment.

A company may believe it’s likely, but not guaranteed, to hit the goal without a SPIF. Or it may conclude that the SPIF will only generate marginal gains. Either way, the core question is one of risk: how confident is leadership that natural sales will hit the target without the SPIF? Deploying a SPIF increases the likelihood of success. Or viewed differently: it lowers the risk of failure.

One of the most important principles of SPIF design is rarity. SPIFs are meant to trigger exceptional effort for exceptional circumstances—a new product launch, a push to hit quarterly numbers, or a kick-start to correct underperformance. They ask reps to shift focus and stretch beyond the usual. But when SPIFs become routine, that effort gets diluted. Reps begin to wait for them. Some may even deprioritize core goals in favor of SPIF-linked deals.

Worse, poorly designed SPIFs can cannibalize natural sales. If a SPIF offers more commission than the base plan, reps may simply redirect existing demand into SPIF-eligible deals. That means the firm isn’t gaining new business—it’s just paying more for sales that would have happened anyway. As one rep recently told us, “Last year I earned over $100,000 from SPIFs—way more than I would’ve made on my core comp plan.” In that case, the SPIFs weren’t special; they had become the system.

And then there’s the matter of expectations. When SPIFs are rolled out on a predictable schedule—say, every year at the end of Q4—reps begin to anticipate them. Sales teams slow their activity in the run-up, waiting for the bonus window to open. And once those bonuses are introduced, they no longer feel like a reward—they feel like an entitlement. As Daniel Pink put it, “Rewards are addictive… before long… it will feel less like a bonus and more like the status quo.”2

At that point, companies often find themselves increasing SPIF payouts just to maintain performance. What started as a short-term motivator becomes a permanent cost center—one that delivers diminishing returns. This is why thoughtful design and disciplined use matter.

A final design criteria focuses on communication. SPIF rules and policies must be clear and cogent. SPIFs do not reach their potential if sales staff invest inordinate time toward understanding the rules rather than making sales calls. Murky documentation can dilute the impact of good sales outcomes. Nothing rankles sales staff more than being denied credit on sales for which they expected commission. Good fences make for good neighbors, and the same goes for SPIF documentation: the clearer the rule set and the SPIF objectives, the less time will be wasted on corner-case eligibility and post-sale disputes.3

A common cause of suboptimal SPIF design is overly narrow thinking. While a focused commercial goal is often a defining feature of a SPIF, that same focus can become a liability if it blinds the organization to broader strategic considerations. This risk is especially pronounced when SPIFs are developed in isolation by Sales or Product teams, without input from Customer Service, Finance, HR, or other stakeholders who bring a broader operational and financial perspective. In contrast, the most effective SPIFs tend to emerge from cross-functional collaboration—where commercial urgency is balanced with enterprise-wide implications.

As we noted earlier, SPIFs always add cost. But when designed thoughtfully, they can deliver meaningful impact without huge expense. The key lies in how the incentive is structured. Most SPIFs are built on a linear model: as sales increase, so do payouts. This straightforward approach is familiar and easy to implement, but it’s not always the most efficient. A more strategic alternative involves asymmetric design – – structuring the incentive so that the firm achieves its top-line goal without harming the bottom line.

One of the most effective ways to achieve this is through contest-style incentives, where only top performers receive rewards. These programs are common in the form of President’s Clubs or elite recognition tiers: they motivate a wide swath of the sales force, but only a few actually earn the reward. The result is powerful—broad engagement paired with concentrated cost. The same logic can be applied to SPIFs by paying a higher commission or bonus to a limited number of top qualifiers. Everyone works harder to compete, but the firm pays only for the few who reach the top.4

Other designs follow a similar logic. For example, a SPIF can be structured to include a performance floor—a threshold that must be met before payouts begin. For example, if a firm typically generates $3 million in sales of a product and sets a goal of $5 million for the quarter, the SPIF might only apply to sales above the $3 million baseline. This avoids paying commissions on sales that would have happened organically, and adds a layer of team motivation: the closer the group gets to the threshold, the more everyone benefits from pushing it over the line.

Importantly, none of these approaches diminish the experience for the sales team. SPIFs are always additive; they exist on top of base variable compensation. No rep is worse off for making a SPIF-qualifying sale—they simply have more to gain. That gives leadership flexibility to design programs that motivate without overspending. In this way, asymmetric SPIFs strike a balance: generous enough to excite, but disciplined enough to protect margin.

Conclusion

Ultimately, the best SPIFs are designed with an ownership mindset. That means asking: How will this program impact the firm’s overall value? What risks are we willing to take to achieve the goal? Not every initiative requires universal consensus—but it does demand a deliberate, objective assessment of whether the SPIF’s cost is justified by its potential impact.

This mindset shifts SPIFs from reactive to strategic, and reframes the question from “What will motivate the team in the short-term?” to “What will add business value over time?” The true cost of a SPIF isn’t just the cash paid out, but also the habits and expectations it forms and the precedent it leaves behind.

When used well, SPIFs can drive the right level of focus, urgency, and performance. Just like that flash sale in the storefront window, they must be simple and designed to move people to act in ways they wouldn’t otherwise. But the moment a flash sale becomes a never ending fixture, shoppers stop seeing it as special. The same goes for SPIFs. The right SPIF, at the right time, for the right reason, is still one of the most powerful levers a sales organization can pull.

SPIF Success Scorecard

Strategic Guide to Effective Sales Incentives

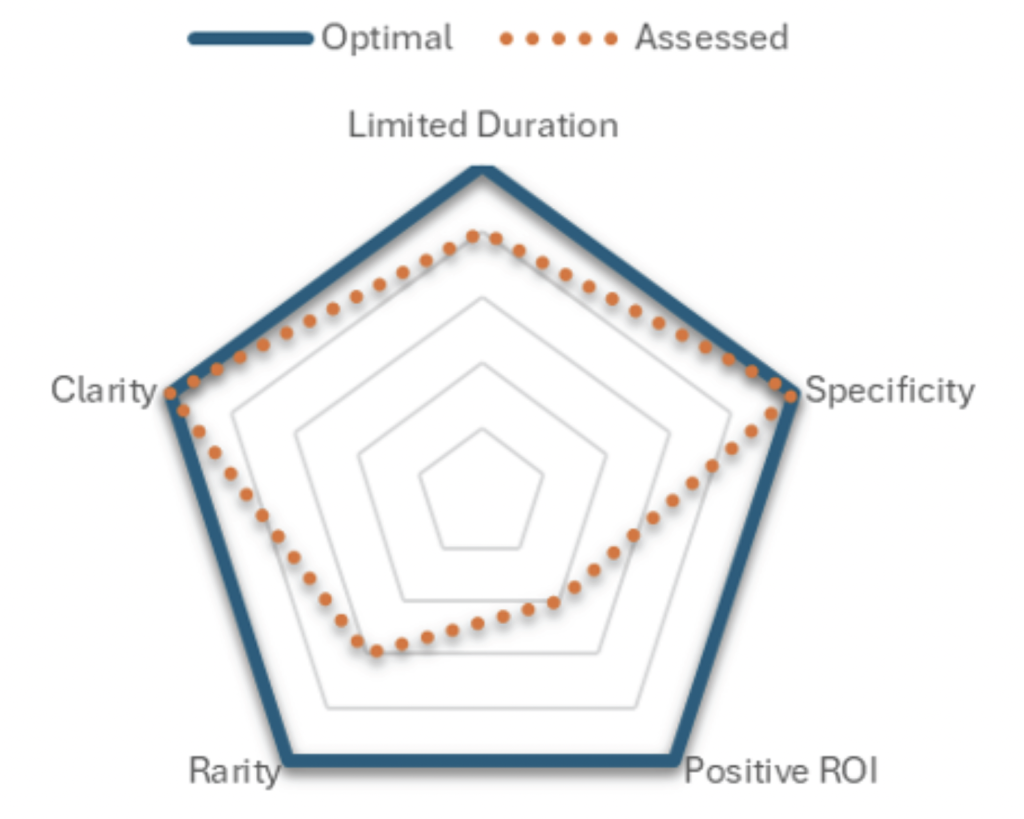

To balance strategic intent with executional discipline, SPIFs should be evaluated using a structured framework. Introducing the SPIF Success Scorecard—a tool that assesses five critical dimensions: Specificity, Limited Duration, Positive ROI, Rarity, and Clarity. Each is scored from 1 to 5. The result is a radar chart that quickly shows whether a SPIF is well-calibrated, needs adjustment, or isn’t fit for purpose. Below we apply this Scorecard to a real-life SPIF example.

Evaluation Criteria & Scoring

| Dimension | 5 (Ideal) | 3 (Moderate) | 1 (Poor) |

|---|---|---|---|

| Specific | 🟢 5: The SPIF targets a specific business objective (e.g., new product launch, clearing excess inventory). | 🟡 3: The goal is somewhat clear but broad or difficult to measure. | 🔴 1: The SPIF is vague, generic, or simply aimed at “boosting sales” without strategic alignment. |

| Limited Duration | 🟢 5: The SPIF has a clearly defined, limited duration (e.g., a month or a quarter). | 🟡 3: The SPIF has an end date but risks becoming a recurring incentive. | 🔴 1: The SPIF lacks a clear timeline and functions as an ongoing bonus. |

| Positive ROI | 🟢 5: The SPIF is projected to generate enough value (revenue, margin, strategic gains) to justify its cost. | 🟡 3: The financial impact is unclear or only marginally positive. | 🔴 1: The SPIF costs more than the benefit it generates, making it unsustainable. |

| Rare | 🟢 5: The SPIF is used selectively as an occasional tool to address specific needs. | 🟡 3: SPIFs are becoming more frequent but still somewhat justified. | 🔴 1: SPIFs are overused, signaling potential issues in the core compensation structure. |

| Clear | 🟢 5: The SPIF is easy to understand, communicate, and track. Sales reps immediately grasp the incentive. | 🟡 3: Some complexity exists, requiring explanation, but the overall concept is clear. | 🔴 1: The SPIF is confusing, difficult to track, or prone to misinterpretation, leading to low engagement. |

Guardrails for Effective SPIF Design

- No Low Scores: If any dimension scores a 1 or 2, reconsider adjusting that aspect of the SPIF before moving forward.

- Balance Over Total Score: A high total score does not compensate for extreme weaknesses in one area. Strive for an even, well-rounded radar graph.

- Iterate and Refine: If a SPIF is imbalanced, adjust its structure and reassess using the scorecard to ensure it aligns with strategic goals.

Final Assessment

21–25 Points: ✅ Green Light – A well-designed, strategic SPIF worth implementing. 15–20 Points: ⚠ Proceed with Caution – Consider adjustments before launch.

Below 15 Points: ❌ Red Flag – The SPIF is likely ineffective or counterproductive.

Applying the SPIF Success Framework: A Real-World Example

To evaluate the effectiveness of short-term sales incentives, let’s consider an example from a large financial services firm that recently launched a new AI-powered product. The company’s goals were aggressive: close 100 deals within two months to secure first-mover advantage and generate buzz for its upcoming quarterly earnings call. To accelerate adoption, the company offered a SPIF that rewarded sales reps a fixed dollar amount for the first 100 deals closed.

| Category | Rationale | Optimal | Assessed |

|---|---|---|---|

| Limited Duration | The SPIF ran for 2 months, which qualifies as short-term. However, a shorter window (4-6 weeks) might have created greater urgency and energy. | 5 | 4 |

| Specificity | The incentive was narrowly focused on a single product, which helped ensure attention and alignment. | 5 | 5 |

| Positive ROI | While the SPIF drove sales volume, it did not exclude replacement sales. As a result, the firm paid commissions on deals that cannibalized an existing solution, undermining incremental gain. | 5 | 2 |

| Rarity | SPIFs were already commonplace at the company, reducing their perceived value and motivational lift. A more infrequent cadence would enhance impact. | 5 | 3 |

| Clarity | The SPIF was easy to understand and communicate, ensuring that reps knew exactly what was required and how they’d be rewarded. | 5 | 5 |

| 25 | 19 |

Based on the SPIF Success Framework, this incentive scored 19 points, therefore falling in the “Proceed with Caution” range. While the SPIF was highly specific and clearly communicated, it fell short in one critical area: return on investment. The incentive paid out on all sales of the new product, including those that simply replaced an existing solution, resulting in minimal net-new revenue. This led to a score of 2 in the ROI category, which is below our recommended threshold. According to our guardrails, any score of 1 or 2 in a single dimension warrants reconsideration or redesign. Despite its strengths, the imbalance created by this weak ROI undermines the overall effectiveness of the SPIF. Before launching, the company should have revised the structure to focus incentives on truly incremental sales in order to better align with strategic goals and preserve financial discipline.

SPIF Scorecard Radar Chart

1 Empirical data is hard to come by to validate this point. One commentator noted that “around 60%” of firms use SPIFs (link below) but doesn’t provide hard data. Our experience is that every incentive compensation design professional we have met works at firms that use SPIFs. Alexander Group, “ Sales Compensation Trends and Mandates,” December 2021, https://www.alexandergroup.com/insights/business-services-podcast-gtm-trends-sales-comp/.

2 D. Pink, “Drive: The Surprising Truth About What Motivates Us,” Riverhead Books, 2023, pg 54.

3 Since SPIFs are created as standalone incentives they are almost never coded into a firm’s commission system but instead are tracked offline. As a result, a SPIF payment may escape clawback if the sale is later disqualified (for example, due to non-payment) because the tracking process doesn’t systematically flag it even when the core commission is. This adds added importance to providing clear documentation in the SPIF rules.

4 An additional benefit to these incentives is that they typically generate a diversity of qualifiers instead of a concentration. Their narrow focus & brief duration allows more ‘randomness’ to occur as many sales reps have the potential to be front runners over a short period. This dynamic fosters motivation and energy behind the initiative.